by: Jack Rasmus, Truthout Sunday 22 May 2011

Every spring for the last three years, the business press and government policy makers declare with great fanfare that the job market in the US has finally turned the corner; sustained recovery in job creation has begun. But every summer following their pronouncements, the opposite occurs: employment and job creation retrenches from the spring and declines.

In recent months, the US Labor Department has reported that jobs for March and April 2011 grew by more than 200,000 each month. Apart from the fact that 130,000 new workers enter the labor force each month, and, therefore, the "net" gain is really only 70,000 (and a third to half of gains represent part time and temp workers), the 200,000 jobs represent an apparent relative improvement over the dismal job creation picture since last June 2010. But appearances are deceptive, and sometimes even false.

How real is the job growth in recent months? And will it continue for the remainder of 2011? Our answer to the first query is "not very" and to the second, "not likely." Here's why.

If the past three years, 2008-2010, are any indicator, employment gains that occur in the spring are not a true, reliable indicator of actual job creation. And the gains of this spring will once again likely disappear in the coming summer-fall of 2011.

The reason has to do with serious problems with the way the Department of Labor calculates employment gains every spring, and in particular, during the second quarter of April-June. When the economy is growing, the problems in calculation are minimal. But when the economy is in a deep downturn, or remains stagnant, the problems are exacerbated.

At the heart of the calculation of employment problem is a practice the US Labor Department employs called the "net new business formation" model, officially called the "Business Employment Dynamics" model (BDM). Every spring, the Labor Department "plugs in" a number of job gains from this model into the Current Establishment Survey (CES), which gathers the actual data on job totals in the economy from more than 400,000 establishments or businesses. The raw data on actual jobs created from the CES is relatively accurate. But the BDM is not. The BDM is not an actual tally of jobs. It is a convoluted "model" that estimates how many jobs are created from the formation of new businesses minus the number of companies going out of business. The numbers for the creation of new businesses, and corresponding new jobs associated with those new businesses, come from state unemployment insurance records that are a minimum of nine months old. And by the time the data is recorded, it is at least one year old. On the other hand, there is no accurate data on the "death" of old businesses. So, the Labor Department takes the number for new businesses, a year ago, and picks a number for "death" of old businesses (for which there are no records), and then plugs the "net" result into the actual number of jobs obtained from the regular CES survey of jobs for the month. But that's not all. The plug-in number is not only from data a year old. It is a historically averaged long run assumed number. So, new business formation from years ago, when the economy was doing well, further upward biases the jobs in the model when the economy is in a deep downturn. The Labor Department itself actually admits, "even in a year where total nonfarm employment declines, the residual net birth-death employment component is positive." We can have a major collapse of small businesses by the hundreds of thousands a month during a recession - which is what in fact happened and still continues to happen - but, nonetheless, the addition to jobs is "positive."

What this all results in is a falsely boosted number of jobs created from the BDM model that are added to the second quarter raw jobs numbers. The spring jobs numbers thus are always heavily inflated.

The Labor Department then takes the model's inflated numbers, adds them to the actual CES raw jobs numbers and then "seasonally adjusts" the combined numbers upward every spring-second quarter. Voila! We get a misrepresented improvement in job creation numbers every spring. But the false boost in job creation in the spring-second quarter declines just as quickly in the summer-fall third quarter when the BDM and seasonality adjustments level off.

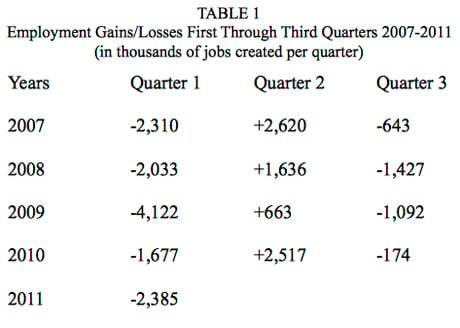

Looking at just the actual, raw jobs data from the CES survey for the second quarter for the last several years, compared to the preceding first and subsequent third quarters, shows how the gains of the second quarter always "run-up" compared to the first and then collapse in the third. This data is from the US Labor Department's CES for the past four years.

When the above raw data from the CES combined with the BDM is subsequently adjusted for seasonality, the result is a rosy picture for job creation in the second quarter radically different from the raw data above for actual jobs created or lost. As Labor Department representatives admitted in a public online question-and-answer session on the BDM model, which this writer attended, "months with generally strong seasonal increases such as April, May, June generally have a larger positive birth-death factor." When that seasonal upward bias disappears in the remainder of the year, jobs then collapse once again.

The problem with the BDM is that it does not reflect any actual job creation data. It is a "model," not an actual survey or census of jobs. It is derived from a long-run historical average for new business creation (and, thus, jobs), which includes economic growth periods when creation is higher than in recessions, when creation may in fact be negative for many months. It does not pick up actual business "deaths" and therefore, job destruction. It is based on data that is lagged at least a full year. It results in a gross overestimation of net new jobs created, and particularly in the spring when seasonality adjustments are factored into the raw data.

What it all means is we can expect a retrenchment on job creation this coming summer once again. Nearly all economic indicators are pointing to a slowdown in the US economy. Housing is in a double dip, with record level collapses in prices, housing starts, sales, and just about everything else. Manufacturing has begun to level off as the global economy slows in turn, with Japan and UK and the Euro periphery in or entering new recessions, and China, Brazil and India taking action to slow their economies. Services growth in the US is also slowing, as the US consumer is hammered by increases in gas and food prices, as well as by continuing double-digit cost increases in health care, education and local taxes. State and local governments are on schedule to lay off at least 400,000 in the coming fiscal year, having sacked 300,000 last year. And the federal government, where jobs have been flat, will lay off hundreds of thousands more if current directions in budget cutting are any indicator.

So, don't get too excited about US government jobs reports in the second quarter. And hold onto your hat. The jobs crisis is far from over.

Every spring for the last three years, the business press and government policy makers declare with great fanfare that the job market in the US has finally turned the corner; sustained recovery in job creation has begun. But every summer following their pronouncements, the opposite occurs: employment and job creation retrenches from the spring and declines.

In recent months, the US Labor Department has reported that jobs for March and April 2011 grew by more than 200,000 each month. Apart from the fact that 130,000 new workers enter the labor force each month, and, therefore, the "net" gain is really only 70,000 (and a third to half of gains represent part time and temp workers), the 200,000 jobs represent an apparent relative improvement over the dismal job creation picture since last June 2010. But appearances are deceptive, and sometimes even false.

How real is the job growth in recent months? And will it continue for the remainder of 2011? Our answer to the first query is "not very" and to the second, "not likely." Here's why.

If the past three years, 2008-2010, are any indicator, employment gains that occur in the spring are not a true, reliable indicator of actual job creation. And the gains of this spring will once again likely disappear in the coming summer-fall of 2011.

The reason has to do with serious problems with the way the Department of Labor calculates employment gains every spring, and in particular, during the second quarter of April-June. When the economy is growing, the problems in calculation are minimal. But when the economy is in a deep downturn, or remains stagnant, the problems are exacerbated.

At the heart of the calculation of employment problem is a practice the US Labor Department employs called the "net new business formation" model, officially called the "Business Employment Dynamics" model (BDM). Every spring, the Labor Department "plugs in" a number of job gains from this model into the Current Establishment Survey (CES), which gathers the actual data on job totals in the economy from more than 400,000 establishments or businesses. The raw data on actual jobs created from the CES is relatively accurate. But the BDM is not. The BDM is not an actual tally of jobs. It is a convoluted "model" that estimates how many jobs are created from the formation of new businesses minus the number of companies going out of business. The numbers for the creation of new businesses, and corresponding new jobs associated with those new businesses, come from state unemployment insurance records that are a minimum of nine months old. And by the time the data is recorded, it is at least one year old. On the other hand, there is no accurate data on the "death" of old businesses. So, the Labor Department takes the number for new businesses, a year ago, and picks a number for "death" of old businesses (for which there are no records), and then plugs the "net" result into the actual number of jobs obtained from the regular CES survey of jobs for the month. But that's not all. The plug-in number is not only from data a year old. It is a historically averaged long run assumed number. So, new business formation from years ago, when the economy was doing well, further upward biases the jobs in the model when the economy is in a deep downturn. The Labor Department itself actually admits, "even in a year where total nonfarm employment declines, the residual net birth-death employment component is positive." We can have a major collapse of small businesses by the hundreds of thousands a month during a recession - which is what in fact happened and still continues to happen - but, nonetheless, the addition to jobs is "positive."

What this all results in is a falsely boosted number of jobs created from the BDM model that are added to the second quarter raw jobs numbers. The spring jobs numbers thus are always heavily inflated.

The Labor Department then takes the model's inflated numbers, adds them to the actual CES raw jobs numbers and then "seasonally adjusts" the combined numbers upward every spring-second quarter. Voila! We get a misrepresented improvement in job creation numbers every spring. But the false boost in job creation in the spring-second quarter declines just as quickly in the summer-fall third quarter when the BDM and seasonality adjustments level off.

Looking at just the actual, raw jobs data from the CES survey for the second quarter for the last several years, compared to the preceding first and subsequent third quarters, shows how the gains of the second quarter always "run-up" compared to the first and then collapse in the third. This data is from the US Labor Department's CES for the past four years.

When the above raw data from the CES combined with the BDM is subsequently adjusted for seasonality, the result is a rosy picture for job creation in the second quarter radically different from the raw data above for actual jobs created or lost. As Labor Department representatives admitted in a public online question-and-answer session on the BDM model, which this writer attended, "months with generally strong seasonal increases such as April, May, June generally have a larger positive birth-death factor." When that seasonal upward bias disappears in the remainder of the year, jobs then collapse once again.

The problem with the BDM is that it does not reflect any actual job creation data. It is a "model," not an actual survey or census of jobs. It is derived from a long-run historical average for new business creation (and, thus, jobs), which includes economic growth periods when creation is higher than in recessions, when creation may in fact be negative for many months. It does not pick up actual business "deaths" and therefore, job destruction. It is based on data that is lagged at least a full year. It results in a gross overestimation of net new jobs created, and particularly in the spring when seasonality adjustments are factored into the raw data.

What it all means is we can expect a retrenchment on job creation this coming summer once again. Nearly all economic indicators are pointing to a slowdown in the US economy. Housing is in a double dip, with record level collapses in prices, housing starts, sales, and just about everything else. Manufacturing has begun to level off as the global economy slows in turn, with Japan and UK and the Euro periphery in or entering new recessions, and China, Brazil and India taking action to slow their economies. Services growth in the US is also slowing, as the US consumer is hammered by increases in gas and food prices, as well as by continuing double-digit cost increases in health care, education and local taxes. State and local governments are on schedule to lay off at least 400,000 in the coming fiscal year, having sacked 300,000 last year. And the federal government, where jobs have been flat, will lay off hundreds of thousands more if current directions in budget cutting are any indicator.

So, don't get too excited about US government jobs reports in the second quarter. And hold onto your hat. The jobs crisis is far from over.

No comments:

Post a Comment